With recent shifts in home prices and mortgage rates in Canada, many Canadians are wondering about the best next steps in their homeownership journey.

Whether you’re a current homeowner or someone considering buying a home, today’s market conditions mean that a well-informed strategy is essential.

In this article, we’ll explore how the current Canadian housing market affects your options, whether you’re thinking about buying, refinancing, or simply assessing your options for the future.

Current State of the Canadian Housing Market

What’s Happening with Home Prices?

Real estate prices in Canada have dropped by 22% over the last 2.5 years. Sourced from wowa.ca.

The Canadian housing market has seen a rollercoaster of price changes over the past few years. In some areas, prices have cooled slightly, while in other regions, home prices remain high due to demand. For those considering buying or selling, understanding these trends is key.

Currently, housing prices are about 22% lower on average across Canada, compared to their peaks in 2022.

Many factors impact Canadian home prices, including economic changes, government policies, and inventory shortages. Current conditions mean that some areas may provide better opportunities for buyers, while others still favor sellers.

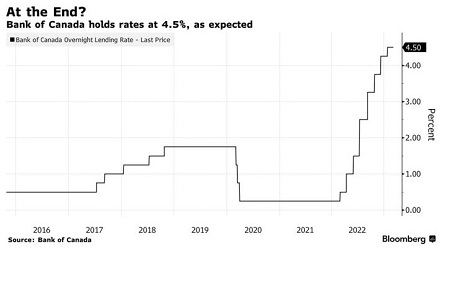

Impact of Mortgage Rates on Buying Power

Home buyer reviewing mortgage rates in Canada

Mortgage rates in Canada have decreased notably over the last 6 months, directly affecting affordability and buying power.

Lower rates mean lower monthly payments, higher affordability, and overall positive impact on what buyers can afford.

Understanding the impact of these rates is essential for anyone considering purchasing a home in today’s market or making changes to their current mortgage.

Considering Buying a Home? Here’s What You Need to Know

Buying a home in a higher-rate environment might seem challenging, but with the right strategies (taking advantage of falling rate), it’s possible to navigate this market and save a lot of money.

Here are a few tips to consider:

Getting pre-approved will give you an accurate picture of how much home you can afford based on current rates.

It’s also a valuable tool for narrowing your search and making competitive offers when you find the right property.

Pre-approval also lets you lock in a rate for a certain period, offering some protection if rates change.

With the market expected to get hot again in the Spring 2025, a pre-approval is a must if you’re planning on buying come April.

Couple considering refinancing their mortgage

Refinancing is a tool that many homeowners use to adjust their finances, whether it’s to secure a lower interest rate, change monthly payment terms, or access home equity for other purposes.

With the recent decrease in mortgage rates, refinancing may be beneficial to your finances (especially if you got your current mortgage in the last 1-2 years).

If your current mortgage has a variable rate and you’d prefer the stability of a fixed rate, refinancing could allow you to lock in a rate for added peace of mind.

Additionally, if you have significant home equity, refinancing can give you access to funds that can be used for home improvements, investments, getting a down payment on another property, and other goals.

Family reviewing Canadian homeownership options

If you’re not quite ready to buy or refinance, that’s okay too! There are still many steps you can take to be prepared when the timing is right. Here are a few: